Vea también

18.10.2024 09:47 AM

18.10.2024 09:47 AM

The Dow Jones Industrial Average hit new highs again, ending Thursday at its fourth all-time high in the last five sessions. The reason for this rise was the results of retail sales in the US, which turned out to be significantly higher than expected, indicating sustainable consumer demand.

Other key Wall Street indices remained generally stable. The S&P 500 slightly rolled back, recording a small loss, while the Nasdaq Composite, on the contrary, was able to show modest growth.

One of the main drivers of positive sentiment in the market was Taiwan Semiconductor Manufacturing Co (TSMC), the world's largest contract chipmaker. The company exceeded analysts' profit expectations and announced a likely jump in revenue in the fourth quarter due to strong demand for chips used in artificial intelligence technologies.

TSMC shares, traded on US exchanges, soared by 9.8%. The company's customer and AI leader Nvidia also saw gains, up 0.9%.

The optimistic sentiment spread to other semiconductor companies, with the Philadelphia SE Semiconductor Index rising 1%, showing broad market support.

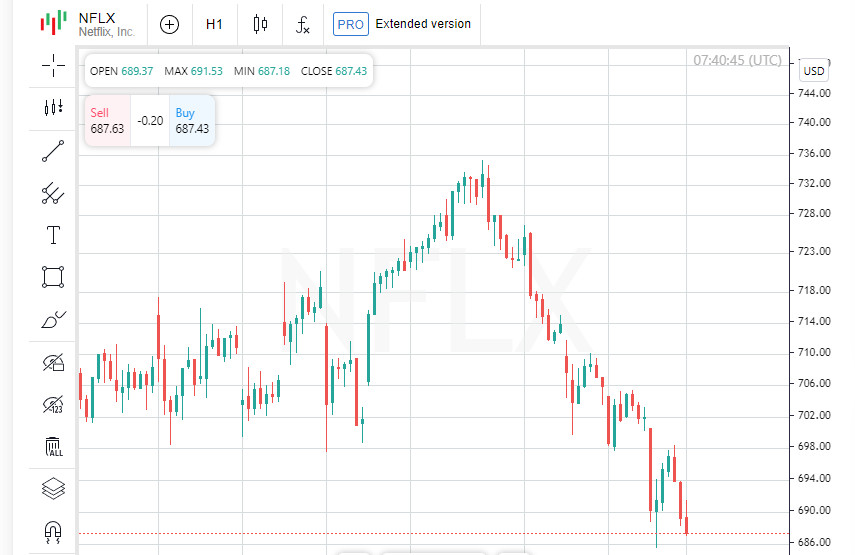

Streaming giant Netflix was also in the mix. The Frankfurt-listed company's shares jumped 4.5% in early trading on Friday, following strong subscriber growth, with the company adding 5.1 million new users in the third quarter, beating expectations by 1 million.

Netflix said it expects to see further subscriber growth ahead of the holiday season, when viewers will once again be able to enjoy the sequel to the popular Korean series "The Squid Game."

Stocks rose 3% in after-hours trading on Thursday, despite a slight 2% decline in the main session, to close at $687.65. The move was a reaction to positive data that bolstered investors' expectations for further growth.

Fresh statistics from the US confirmed the stable development of the world's largest economy. Retail sales increased by 0.4% in September, which was slightly higher than expected. In addition, the number of jobless claims unexpectedly fell, which also increased confidence in the stability of the labor market.

However, despite the improving economic data, forecasts for a 25 basis point interest rate cut at the next Federal Reserve meeting remain unchanged — 89.4%, according to FedWatch CME.

The start of the third-quarter reporting season also added to the optimism. Strong economic data and prospects for easing by the Federal Reserve helped the Dow and S&P 500 continue their climb to record highs. The S&P 500, in particular, is approaching the significant psychological boundary of 6,000 points.

The S&P 500 index ended the day slightly down 1 point, or 0.02%, reaching 5841.47. At the same time, the Nasdaq Composite rose 6.53 points, or 0.04%, to close the session at 18373.61. The Dow Jones Industrial Average showed a more confident increase - by 161.35 points, or 0.37%, to close the day at 43239.05.

Josh Jamner, an investment strategy analyst at ClearBridge Investments, noted that current economic data has changed investors' views. Strong data has eased fears of a possible recession, leading to a revision of expectations for further economic growth and corporate profits.

After months of gains in the largest companies, investors continue to look for sectors and companies to invest in for further growth. Despite the overall improvement in the market, choosing the right time and direction for investments remains a challenge.

"The market continues to rise, but more subdued than one would expect," said Josh Jamner of ClearBridge Investments.

The Russell 2000 Index lost 0.3%, while the S&P Small Cap 600 fell 0.2%. This happened the day after both indexes reached their highest in almost three years. This points to weakness in small-caps, which could signal a more cautious mood among investors.

Most sectors in the S&P 500 index also showed negative momentum. Interest-rate-sensitive sectors such as utilities and real estate were particularly hard hit, falling 0.9% and 0.7%, respectively. Rising U.S. Treasury yields are putting pressure on companies with high leverage, hurting their stocks.

In an unusual move in recent days, U.S. stock indexes have been rising alongside rising Treasury yields. On Thursday, the 10-year yield rose 7.5 basis points to 4.091%. This could signal stronger inflation expectations and tighter financial conditions.

Travelers Companies and Blackstone Group posted strong gains of 9% and 6.3%, respectively, following the release of their third-quarter earnings reports. Both giants beat market expectations for profits, spurring interest in their stocks.

The S&P Banks Index extended its gains, adding 0.1% to reach its fifth straight session of gains, its best streak since August and one of the few such extended gains since April. Large regional banks reported third-quarter results, helping to bolster investor confidence in the banking sector.

With positive corporate earnings reports and rising bond yields, investors continue to watch the market closely to see which sectors and companies will be on the rise in the coming months.

M&T Bank and Synovus Financial were solid gainers, jumping more than 5%. Not all banks followed suit, however, with Truist Financial down 3.5% and Huntington Bancshares down 2.6%. The mixed picture highlights how financial institutions are coping differently with the current market conditions.

Outside the financial sector, Elevance Health, a leading health insurer, plunged 10.6%. It was the company's biggest one-day drop since March 2020, when the world was grappling with the pandemic. The decline came after the company lowered its full-year profit guidance, causing a wave of investor concern.

Trading volume on U.S. exchanges totaled 11.34 billion shares, below the 12.08 billion average over the past 20 trading days. This could indicate that investors are becoming more cautious as they analyze incoming quarterly reports and await further economic data.

While the Dow Jones Industrial Average ended Thursday at a record high, the S&P 500 and Nasdaq ended the session little changed, giving up some of their daily gains. Investors digested mixed quarterly earnings and positive economic data that created a mixed market sentiment.

Amid growing uncertainty surrounding the upcoming US elections, gold, the traditional safe haven asset, soared to record highs. Investors flocked to the safe haven, strengthening the precious metal's position in the market.

The technology sector, and chip-related companies in particular, beat analysts' expectations. Taiwan Semiconductor Manufacturing (TSMC) reported strong earnings and forecast a strong rise in fourth-quarter revenue, allaying concerns about a potential slowdown in chip demand.

TSMC has been a major contributor to the recent market rally, with its positive outlook reassuring investors worried about a potential slowdown in the semiconductor sector. Expectations of a glut due to the rise of AI have not been borne out by the company's orders. "TSMC continues to show solid demand, which is giving strength to the entire sector," said Michael Green, chief strategist at Simplify Asset Management.

Green also added that the leadership of large-cap semiconductors will be a catalyst for the major indices. In addition, the positive reaction to retail sales data also supported the U.S. market.

The S&P 500 closed with minimal losses, while the Nasdaq managed to end the day with a small gain. This came as strong retail sales and low jobless claims failed to drive the gains that investors had expected.

Growth stocks continued to outperform value stocks, with regional banks leading the pack as upbeat earnings from players like M&T Bank and KeyCorp gave the sector a boost.

European stock markets also rose, closing within 1% of their all-time highs after the European Central Bank (ECB) cut its interest rate by 25 basis points as expected. However, the ECB gave no clear direction on what to do next.

The ECB's third rate cut this year reflects a shift in priorities: from fighting inflation to supporting the weakened economy of the European Union, raising expectations about the regulator's future actions.

The MSCI share index, which reflects global stock markets, rose by 0.02%, or 0.21 points, to 852.43. European stock markets also ended the day on a positive note: the STOXX 600 index added 0.83%, and the FTSEurofirst 300 rose by 17.82 points, or 0.87%. Meanwhile, emerging markets showed less optimistic results: the MSCI Emerging Markets index fell by 0.78%, losing 8.88 points and falling to 1,135.16.

Treasury yields rose after data that confirmed the strong fundamentals of the U.S. economy, leaving the Federal Reserve room to move more cautiously on interest rates. The yield on the 10-year note rose 8.2 basis points to 4.098%, up from 4.016% the day before.

The 30-year note also increased its yield by 9.8 basis points to 4.3972%, while the two-year note, which is most sensitive to interest rate expectations, rose 4.8 basis points to 3.983%.

The U.S. dollar strengthened, hitting an 11-week high, amid retail sales data that beat analysts' expectations. This increased investor confidence in the stability of the U.S. economy. The dollar index, which tracks the dollar against its major counterparts, rose 0.24% to 103.79. The euro, by contrast, fell 0.3% to $1.0828.

The U.S. dollar rose 0.41% against the Japanese yen to 150.23, reflecting investor confidence in the stability of the U.S. economy and heightened expectations for the Federal Reserve's future policy.

Oil prices rose slightly, reflecting a difficult market environment as investors navigate geopolitical risks related to the conflict in the Middle East and data showing a decline in U.S. crude inventories. US crude oil rose 0.40% to $70.67 per barrel, while Brent crude rose 0.31% to end the day at $74.45 per barrel.

Gold continues to break records, adding 0.7% to $2,691.97 per ounce. This growth is associated with expectations of possible interest rate cuts by the Federal Reserve, as well as growing uncertainty around the upcoming US presidential election. Investors see gold as a safe haven asset amid global turbulence.

You have already liked this post today

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.